In this article, we explain what a SAFE Note is, how it works, its main features, when it is recommended, and the key differences compared to a convertible note. In addition, we discuss accounting and tax treatment in Spain, numerical examples of conversion, and the changes introduced by the Startups Act (Law 28/2022).

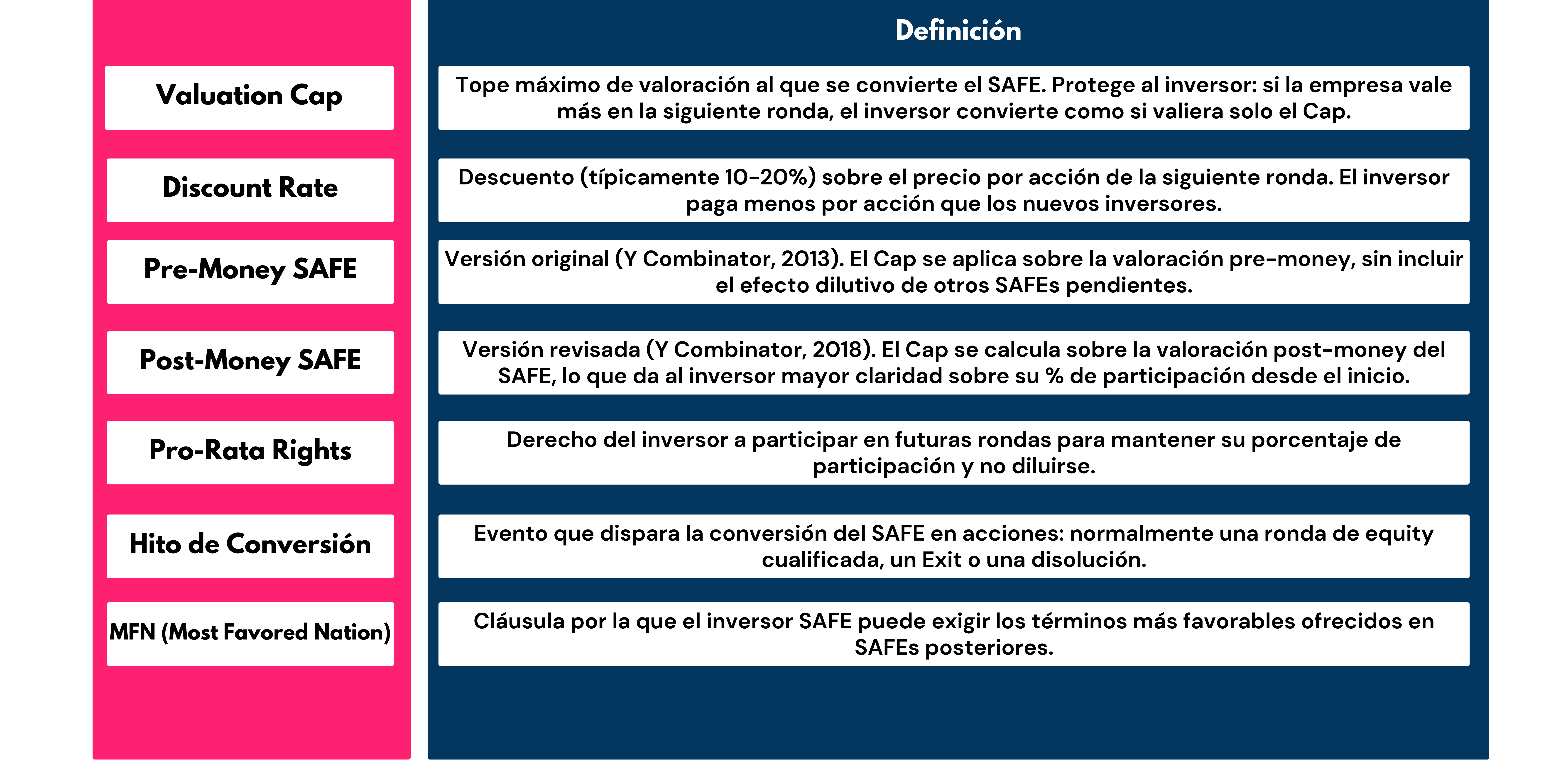

Quick Glossary: Essential Safe Note Terms

Before getting into the subject, you should define the terms you'll find throughout this guide:

What is a SAFE Note and what are its main features?

A SAFE Note is an agreement by which an investor provides funding to a startup in exchange for rights to shares that will be issued in the future. Its distinctive feature is simplicity: it does not require an immediate assessment of the company. Instead, SAFE is converted into shares in a subsequent round, generally applying a discount or valuation cap. This structure reduces the complexity of initial negotiations and is attractive to both entrepreneurs and angel investors and seed-phase venture capital funds.

Origin of SAFE: Pre-Money (2013) vs. Post-Money (2018)

In 2013, the American accelerator Y Combinator introduced the first version of SAFE, based on a pre-money assessment. In 2018, it revised the instrument and launched the Post-Money SAFE, today the most used in the market.

The difference is critical for Spanish investors:

- Pre-Money SAFE (2013): The final investor percentage is uncertain until the round is closed, because it depends on how many other SAFES are converted simultaneously. The cumulative dilution is not visible from the start.

- Post-Money SAFE (2018): The investor knows exactly what percentage he will get from the moment of signing (Investment ÷ Valuation Cap =% of participation). This gives founders and investors much more clarity about the dilution before the equity round. This version is currently preferred by most investors in Spain.

💡 Why does this distinction matter in Spain? An investor who contributes 100,000€ in a Pre-Money SAFE with a Cap of 2M€ could end up with 4%, 3.5% or less depending on how many other SAFEs are accumulated. With Post-Money SAFE: 100,000€/2,000,000€ = exactly 5%. No surprises. Spanish institutional investors and family offices are increasingly demanding the Post-Money version for this reason.

How does a SAFE Note work? Real numerical example

The operation is straightforward: the investor provides capital today, and that capital is converted into shares when the conversion milestone occurs. Let's look at a complete example:

Conversion scenario with Valuation Cap

📊 Practical example of SAFE conversion

Data: Startup receives €100,000 through SAFE with a Cap of €2,000,000 and a 20% discount.

Scenario A — Series A Round at a pre-money valuation of €4,000,000:

• Price per share in the round: €4,000,000/1,000,000 shares = €4/share

• SAFE Price per Cap: 2,000,000€/1,000,000 shares = 2 €/share

• SAFE Discount Price: 4€ × (1 - 20%) = 3.20€/share

→ The most favorable one applies: 2€/share (per Cap)

→ The SAFE investor receives: 100,000€/2€ = 50,000 shares

→ New investors in the round would pay 4€/share (50% more expensive)

Scenario B — Series A Round at a pre-money valuation of 1,500,000€ (below the Cap):

• Price per share in the round: 1,500,000€/1,000,000 shares = 1,50€/share

• SAFE Discount Price: 1.50€ × (1 - 20%) = 1.20€/share

→ The most favorable one applies: 1.20€/share (discount acts because Cap doesn't apply)

→ The SAFE investor receives: 100,000€/1,20€ = 83,333 shares

Conversion and liquidity events

SAFE is activated in the face of three types of events:

- Qualified equity round: The company closes a funding round that exceeds a minimum threshold (typically defined in SAFE itself). This is the most common conversion event.

- Exit (sale of the company): If the company is acquired before the equity round takes place, the SAFE investor can choose between receiving the amount of their investment or converting to the Cap and receiving their proportional share of the sale price. This is agreed in the SAFE liquidity clause.

- Dissolution: If the company dissolves without having closed a round or an Exit, the SAFE investor has priority over the founding partners (but not over creditors) to recover their investment. This differentiates it from a simple equity right from the start.

Legal Framework in Spain: Is the SAFE Note legal?

Is the SAFE Note legal in Spain?

Yes. The SAFE Note is an atypical private contract that is fully valid in Spain under the principle of autonomous will (Article 1255 of the Civil Code). However, since the Spanish legal system is of continental origin (unlike the Anglo-Saxon one where SAFE was born), there are some peculiarities:

- Private contract vs. security value: A SAFE in Spain is usually formalized as a private contract. It does not require public deeds to be valid, although some investors prefer to make it public (notarial record of statements) for greater legal security.

- Notary file: If it is decided to raise the SAFE to a public document, the notary records the existence of the agreement without qualifying it as a security instrument. This adds security without requiring the complexity of a formal capital increase.

- CNMV and MiFID II: SAFEs between qualified investors (business angels, family offices, VCs) are generally outside the scope of CNMV supervision. For SAFES with unqualified individuals, restrictions may apply under crowdfunding regulations (EU Regulation 2020/1503).

Startups Act (Law 28/2022): impact on the SAFE Note

Law 28/2022 on the promotion of the ecosystem of emerging companies (“Startups Act”) introduces several facilities directly relevant to SAFES:

- Stock options and deferred equity: The law improves the tax treatment of stock options, which complements the use of SAFE as an instrument for raising capital at an early stage.

- Special tax regime for startups: Companies that obtain the “start-up” seal (granted by ENISA) have access to advantages such as the reduced rate of 15% in IS for the first four years with a positive tax base, deferred payment of IS in the first two years and easy taxation for members.

- Visa for digital nomads and investors: The law makes it easier to attract foreign capital and investors, expanding the pool of potential SAFES signatories in Spain.

- Deduction for investment in newly created companies (Art. 68.1 LIRPF): This deduction (up to 50% of the amount invested with a maximum of 100,000€ per year) is applied to the acquisition of shares or shares. SAFES, since they are not yet shares at the time of signing, do not allow this deduction to be applied directly. The deduction applies when SAFE converts into shares, provided that the requirements are met at that time

Accounting and tax treatment of SAFE Note in Spain

How is a SAFE recorded on the balance sheet?

This is one of the most debated and least explained issues in articles on SAFES in Spain. The SAFE accounting classification has direct implications for the faithful image of the balance sheet and the debt-to-equity ratio that future investors will see:

What are the key differences between a SAFE Note and a convertible note?

Choosing between SAFE and convertible notes conditions the investor-startup relationship and the financial terms of the agreement. This is the extended comparison:

💡 SAFE + ENISA: are they compatible? A frequently asked question is whether a SAFE coexists with an ENISA participatory loan. The answer is yes, but with nuances. ENISA usually requires that the startup have a minimum of own funds and may consider SAFE as a liability (not as own resources) in its analysis. It is recommended that the SAFE be signed and the capital transferred before applying for the ENISA loan, and to ensure that the accounting classification is consistent with the requirements of the ENISA evaluator.

Step-by-step process: how to sign a SAFE Note in Spain

The process in Spain has peculiarities compared to the Anglo-Saxon model. Here is the usual flow:

- Negotiating terms: Agreement on the amount, the Valuation Cap, the Discount Rate, if it includes Pro-Rata Rights and MFN clause. In Spain, the usual practice is to adapt Y Combinator's Post-Money SAFE model to the Spanish legal system.

- Drafting of the private contract: The lawyer drafts the contract in Spanish, adapting the Anglo-Saxon SAFE. It is recommended to include clauses on: applicable (Spanish) legislation, competent courts, local liquidity events and treatment in the event of bankruptcy.

- Signing of the contract: Advanced electronic signature (e.g. Signaturit, DocuSign) or in-person signature. Both are fully valid in Spain.

- Transfer of capital: The investor makes the bank transfer to the startup's account. This movement is recorded as extraordinary income until conversion.

- Notarial statement of statements (optional but recommended): Raising SAFE to a public document by means of a notarial act provides greater legal security. It's not mandatory, but investors with tickets over 100,000€ usually request it.

- Accounting record: The startup records the amount received in the balance sheet as a non-current liability (PGC account 179) or deferred equity instrument, according to accounting criteria agreed with the auditor.

- Conversion into shares: When the conversion milestone (qualified equity round) occurs, SAFE automatically converts. The startup issues new shares or shares in favor of the SAFE investor through a notarial public decree and registration in the Mercantile Registry.

When is it recommended to use a SAFE Note?

The SAFE Note is especially useful in the following scenarios:

- Pre-seed and seed funding with angel investors: When the startup is uncertain about its valuation and needs quick capital without the costs of a formal equity round.

- Rolling closes in seed rounds: SAFE allows investors to close progressively without having to wait until all the investors in the round are closed simultaneously.

- Bridge financing: For startups that need to extend their runway while preparing for a Series A round, SAFE is more agile than renegotiating debt terms.

- International investors with Anglo-Saxon familiarity: Business angels from the UK, US or Nordic markets are often familiar with the SAFE format, reducing the trading curve.

Conversely, SAFE may not be the best option if:

- The startup has a clear valuation and wants the investor to enter directly into the cap table from the start.

- The investor requires return guarantees or expiration date (in that case, the convertible note is more suitable).

- The startup has no clear prospects of closing an equity round in the next 12-24 months (SAFE would be suspended indefinitely).

Benefits and risks of the SAFE Note for startups and investors

Advantages

- Simplicity: 5-8 page contract vs. 30-50 pages of a full term sheet. Legal costs from €500 vs. €3,000-8,000 in formal rounds. High impact

- Velocidad: Close in 1-2 weeks vs. 2-3 months in an equity round. Essential when the runway is tight. High impact

- Without immediate dilution: Founders don't dilute their cap table until the conversion, maintaining control in the most critical phase. High impact

- Flexibility of terms: Cap, discount and clauses are negotiable without the need to modify statutes or hold a meeting. Medium impact

- Attractive to investors: The investor enters with protection (Cap) and discount without the complexity of negotiating valuation. Medium impact

Risks

- Cumulative dilution not visible (Pre-Money SAFE): If the startup signs multiple Pre-Money SAFES, the total dilution of the founders in the next round may be much higher than expected. Post-Money SAFE solves this problem.

- Dependency on future rounds: If the startup does not close a qualified equity round, SAFE is suspended indefinitely. For the investor, this can mean fixed capital for years.

- Uncertainty in the face of early exit: Without a well-drafted liquidity clause, the treatment of SAFE in a sale of the company can generate conflicts. It is essential to include this clause explicitly.

- SAFES concentration risk: A startup with a lot of accumulated SAFEs can reach a Series A round with a highly diluted cap table before opening the round, which can dissuade institutional investors.

Advanced Legal Considerations

For readers with legal or financial experience, these are the most technical aspects to consider when structuring a SAFE in Spain:

- Qualification as a financial instrument: According to the CNMV's opinion, SAFES aimed at unqualified investors could fall under the scope of application of the Securities Market Act. It is recommended to limit SAFES to accredited or qualified investors to avoid registration and prospectus obligations.

- Bankruptcy treatment: In the event of bankruptcy of the startup, the SAFE investor is considered a subordinate creditor (similar to the partners) according to the Spanish Bankruptcy Law, which means that they collect after ordinary creditors. This subordination is relevant for investors who value priority in adverse scenarios.

- Anti-dilution in SAFes: Unlike formal round term sheets, standard SAFES do not usually include anti-dilution clauses (broad-based weighted average or ratchet). If the investor requires them, they must be negotiated explicitly.

- Startup Tax Regime (IS): The amount received through SAFE is not considered income for the startup until the conversion. It does not generate a corporate tax base at the time of signing.

Frequently Asked Questions (FAQ)

Is the SAFE Note legal in Spain?

Yes. It is a private contract valid under Article 1255 of the Civil Code. It does not require a public deed, although it can be raised to a notarial document for greater security.

What if there isn't a subsequent round?

SAFE is put on hold indefinitely. There is no obligation for a return on the part of the startup unless there is an Exit or a dissolution. This is the main difference with the convertible note, which does have an expiration date.

SAFE notary registration: when is it necessary?

It is not mandatory, but it is recommended for tickets greater than 50,000-100,000€, when the investor is a family office or institutional fund, or when there is a willingness to raise the agreement as evidence in the face of possible litigation.

SAFE Note vs. Convertible Note: Which One Is Best for My Startup?

It depends on the investor's profile. If the investor is comfortable with no return guarantees and wants simplicity: SAFE. If the investor requires a due date, interest and greater legal protection: convertible note. For very early-stage startups, SAFE is generally more agile and less expensive.

Does the SAFE Note entitle you to a 50% deduction (Art. 68.1 LIRPF)?

Not at the time of signing. The deduction applies when SAFE converts into shares or shares of the company, provided that the deduction requirements are met at that time (start-up company, minority interest, etc.).

Can a SAFE live with an ENISA loan?

Yes, but we must manage the accounting classification well. ENISA analyzes the startup's own resources. If SAFE is classified as a liability, it does not count as equity and may affect eligibility or the amount of the loan. We recommend consulting with an external CFO before combining both instruments.

Conclusion

The SAFE Note is a powerful tool for raising capital at an early stage in Spain. Its simplicity, closing speed and flexibility have made it the favorite instrument of business angels and seed funds in the Spanish ecosystem. However, to use it properly, it is essential to:

- Choose between Pre-Money and Post-Money SAFE according to the investor's needs for clarity.

- Understand accounting and tax treatment in Spain, especially in relation to the Startups Act.

- Include well-written liquidity clauses for Exit or Dissolution events.

- Manage the accumulation of SAFES properly so as not to reach Series A with an excessively diluted cap table.

At Intelectium, as an external CFO specialized in technology startups in Spain, we help founders and investors to structure SAFES correctly, from the negotiation of terms to the conversion into shares. If you have questions about how to structure your seed round, contact our team.